Revelations, 2:11

We Shall Be Patient

Of course, we were all secretly hoping for a barrage of good news and contracts

We didn’t get that….at least directly. Let’s parse some words and see the revelation within.

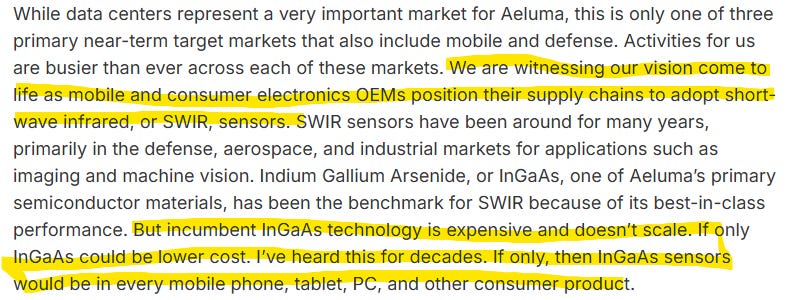

As my daughter would say, “What the?” Why are mobile and consumer electronics OEMs positioning their supply chains to adopt SWIR sensors if SWIR is expensive and doesn’t scale?

Is Aeluma the reason that the supply chains are being positioned to adopt SWIR? Is it because those 20 Apple engineers following ALMU have come to the conclusion that ALMU can scale SWIR sensors for the mass market? Cause or effect? Let’s parse on.

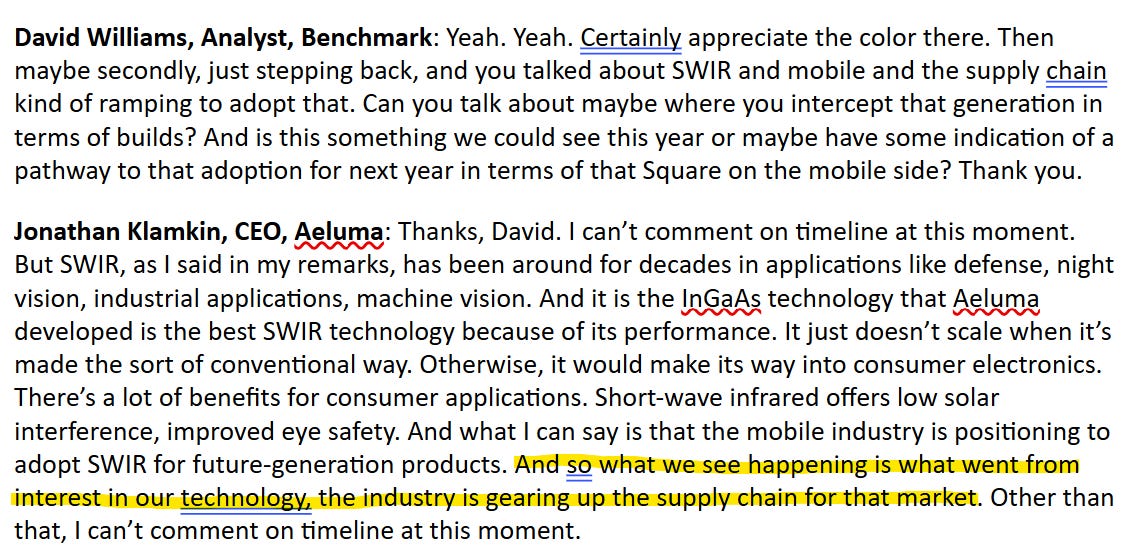

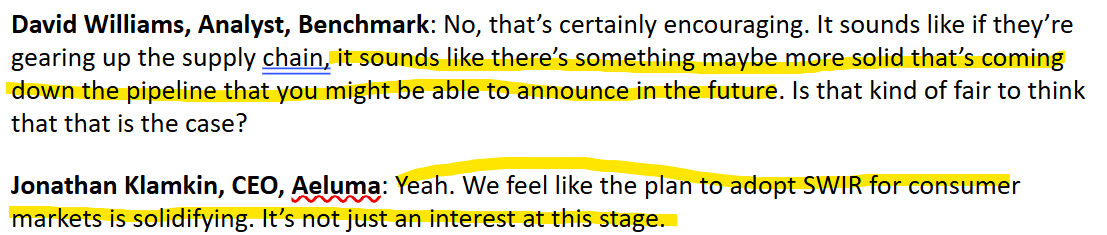

I don’t need to be smacked about the head and neck to see the connection here. There was previously interest in their technology, and now the industry is gearing up the supply chain to use that technology.

But wait….are you sure about that Jonathan?

Let’s wrap this up—we see loads of Apple people following Aeluma. We see Sony investment people following Aeluma. We are told during the Fireside Chat that Aeluma is pursuing partnerships and the mobile timeline is clear now. We hear yesterday that the supply chain is gearing up for SWIR sensors in consumer devices. Am I just a fanboy or is this not obvious to everyone?

What Else?

We know that some form of InGaAs on Si sensor has passed GR-468 qualifications based on the company’s own datasheets. Qualification is no longer a worry of mine. It will happen with each unique product, but we still have no idea on timing. Patience. How about yield?

During the quarter, we continued to increase operations with foundry partners and are delighted with the performance, quality, and yield of wafers being tested at Aeluma’s facility…Chips are yielding and performing as we qualify our processes for target markets.

If Jonathan is delighted, I guess I will also be delighted. Check off the yield worry.

Government awards?

Additionally, we received several award notices recently for later-stage R&D efforts and transition opportunities, reinforcing confidence in Aeluma’s technology and expectations for additional contracts this year.

More coming. Three to seven new development contracts. From the 10-Q…As of December 31, 2025, total remaining performance obligations under all obligated government contracts amounted to $7.9 million. Check.

Data centers?

This is a significant market opportunity now and for the next several years. It is also an opportunity for new technology and product introduction. Higher performance is needed, higher volumes are needed, and cost is critical. The Aeluma platform wins on all of these metrics.

Check.

Quantum?

we believe our platform has more potential than those developed by major quantum system companies. Compared to alternatives such as lithium niobate or barium titanate, Aeluma’s heterogeneous integration on silicon may provide the path forward to scalable quantum photonic systems.

Check.

Defense?

Although mentioned as one of the three primary foci, I didn’t hear any details.

No check.

The Cold Reality of the 10-Q

There was zero commercial revenue recognized in the quarter. There was only $41,000 in the quarter before that. The fanboy in me doesn’t care much because I would give away product to Apple and Infinera to evaluate. Seems to have worked. That means these small “sales orders” showed up after December 31st so we have to wait until the next 10-Q to see how small is small. But again, if they gave away samples that cause Apple to ramp up the SWIR supply chain, I am all for it.

There was some issue with registration of stock that led to the flurry of filings lately. The company would on the hook for damages up to 8% of the shares covered by the registration rights agreement. Someone fucked up. It seems like they dodged a bullet here but somebody was twisting their arm.

The Company currently expects to satisfy all of its obligations under the Registration Agreement and does not expect to pay any damages pursuant to this agreement; therefore, no liability has been recorded.

On a positive note, the going concern language is now all puppies and rainbows for at least 12 months

With the successful completion of the offerings, we believe that substantial doubt about our ability to continue as a going concern has been alleviated for at least the next twelve months.

The bane of small companies, disclosure controls and procedures, were deemed not effective, again. They hired a CFO and bolstered the finance department to fix these issues over time.

F you 10b5-1!

I hate these things, but here we go again. Poor-judgement DenBaars is listed again with his 100,000 potential sale as we saw in the proxy before. Unfortunately, our CEO and founder has filed to sell 150,000 shares. Bummer. He can sell up to September 2, 2026. Poor optics. Borrow against your shares Jonathan. Any investment bank can set that up for you. Selling with zero commercial revenues is just ugly and fodder for short fools.

We are witnessing our vision come to life

If that is true, one would never sell a single share.

So, what do you think are the likely outcomes? Gov R&D contracts keep coming through 2026 to keep the company afloat, but they fold in 2027 if they don't get off the runway with commercial partners?

What do you think the odds are for the largest tech firms who know the specifics of Aeluma's capabilities thinking they can starve the company to death for want of commercialization and delay product integration until they can acquire either all of Aeluma or just its IP?